Toronto sees sharp surge in ultra-rich buying up the most expensive homes

The last year or so may have been a complete flop for Toronto area real estate, but there is one housing type that has been seeing sales soar as others face a grim decline in buyer interest and a flood of listings from increasingly desperate sellers.

In complete contrast to the region's condo market, luxury condos, townhouses, and mansions are hotter-than-ever commodities among the ultra-rich, with activity jumping double-digit percentages in 2024, according to a new report on the best of the best properties from RE/MAX.

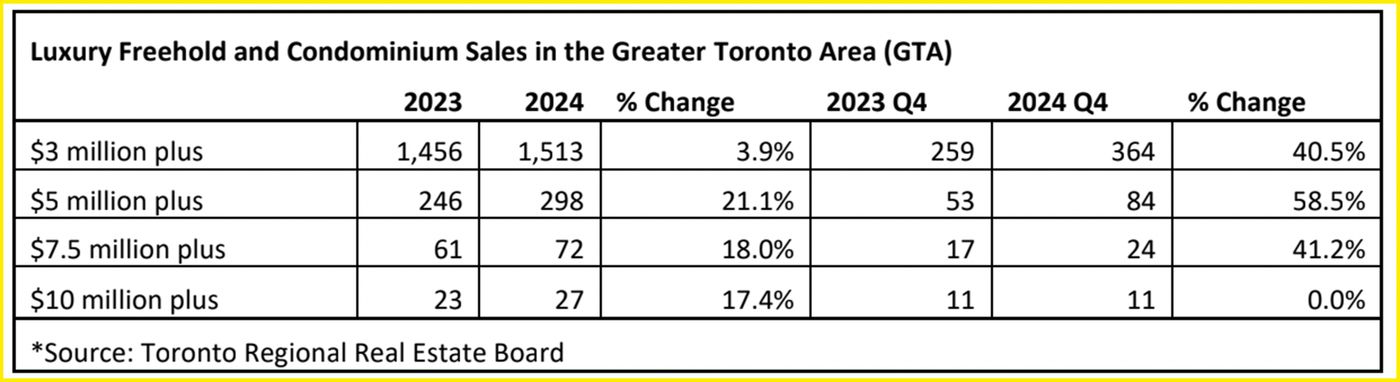

During the last three months of the year, GTA homes in the $5 million to $7.5 million range saw the biggest frenzy, with 58.5 per cent more of them changing hands than during the same few months of 2023.

The ultra-rich are back to buying up mansions no one else can afford in Toronto https://t.co/fAOp5R6Qsc

— blogTO (@blogTO) January 18, 2024

Residential properties between $7.5 million and $9.99 million — unimaginable to the vast majority of locals — saw a similar uptick in sales, of 41.2 per cent year-over-year, as did homes between $3 and $4.99 million, sales of which increased by 40.5 per cent.

Of the area's luxury segment, only estates above the $10 million mark saw no change in the amount of activity from the final quarter of 2023 to the same time in 2024. But, looking at the year as a whole, these over-the-top homes were surprisingly in-demand for those who could afford them.

A total of 17.4 per cent more of this highest echelon of homes were sold last year than over the course of 2023 — not far behind the 18.0 per cent increase in sales of homes between $7.5 million and $9.99 million from one year to the next, and the 21.1 per cent rise in sales between $3 and $4.99 million during the same period.

RE/MAX's report on luxury real estate in the GTA, published Wednesday, shows how the segment has bucked the trend of the region's market generally in the last year.

In Toronto proper, RE/MAX writes that buyers were happily able to "take advantage of suppressed housing values, particularly at uber-luxe price points between $5 million and $7.5 million," with 53 per cent of all of these hundreds of high-end sales taking place within the city's bounds.

But, the number of sales taking place on the outskirts of the city, though lesser than within it, did climb substantially in 2024.

The easing of mortgage lending rates in the last 12 months is noted as a factor in this flurry of transactions, with RE/MAX writing that "the 100-basis-point drop in the overnight rate was the primary catalyst behind stronger buyer enthusiasm," along with more ideal market conditions, buyer confidence and stock market successes compared to 2023.

But, those eyeing homes of this value in and around Toronto are likely above the influence of overvalued pricing, interest rates and the rising cost of living in general that has hampered the remainder of the population and prevented them from buying the cheapest of condos (or for some, being able to afford rent or food), let alone a $10 million mansion.

Arameh Hacopian/Shutterstock.com

Latest Videos

Latest Videos

Join the conversation Load comments